The India You Think You’re Visiting

What overseas cohorts misunderstand, until the first taxi ride, QR code, and risk meeting

The first misconception arrives before the first meeting.

A visiting cohort lands in Bengaluru or Mumbai, steps into a taxi, and experiences the opening lecture: three lanes behaving like five, an orchestra of horns, and a driver who appears to negotiate physics by persuasion. “So chaotic,” someone says, as if they’ve discovered the country’s operating principle.

Twenty minutes later, that same taxi driver stops for tea. The cohort watches him pay by scanning a QR code. No wallet, no change, no drama. A soft ping. Done. The country that looked “unmanaged” in traffic suddenly looks highly engineered in commerce.

India has a habit of doing that: seeming disorderly up close while running systems at scale that many “orderly” countries still debate in committees.

Field immersion corrects misconceptions quickly because India does not explain itself through brochures. It explains itself through contradictions that work.

Misconception 1: “India is one market.”

Reality: it is a federation of operating models.

Executives arrive with a single-market mental model. One India strategy, one India rollout, one India customer. It takes about three conversations to unlearn that.

India is not merely diverse in language and culture; it is diverse in policy pace, infrastructure maturity, and consumer behaviour across states and cities. A distribution plan that looks elegant on a national map often collapses at district level, where procurement norms, local competition, and talent availability differ sharply.

The correction comes fastest when cohorts visit outside the “usual three” metros. A Tier-2 manufacturing cluster teaches different lessons than a Mumbai fintech. A southern services hub behaves differently from a northern consumption belt. The managerial takeaway is not “localise marketing.” It is deeper: design your operating model for variability, because variability is the stable feature.

Misconception 2: “India is low-cost.”

Reality: it is high-expectation, and increasingly high-spec.

The low-cost narrative survives because it is convenient. It also blinds visitors to a more interesting reality: India is building capability at scale and tightening expectations.

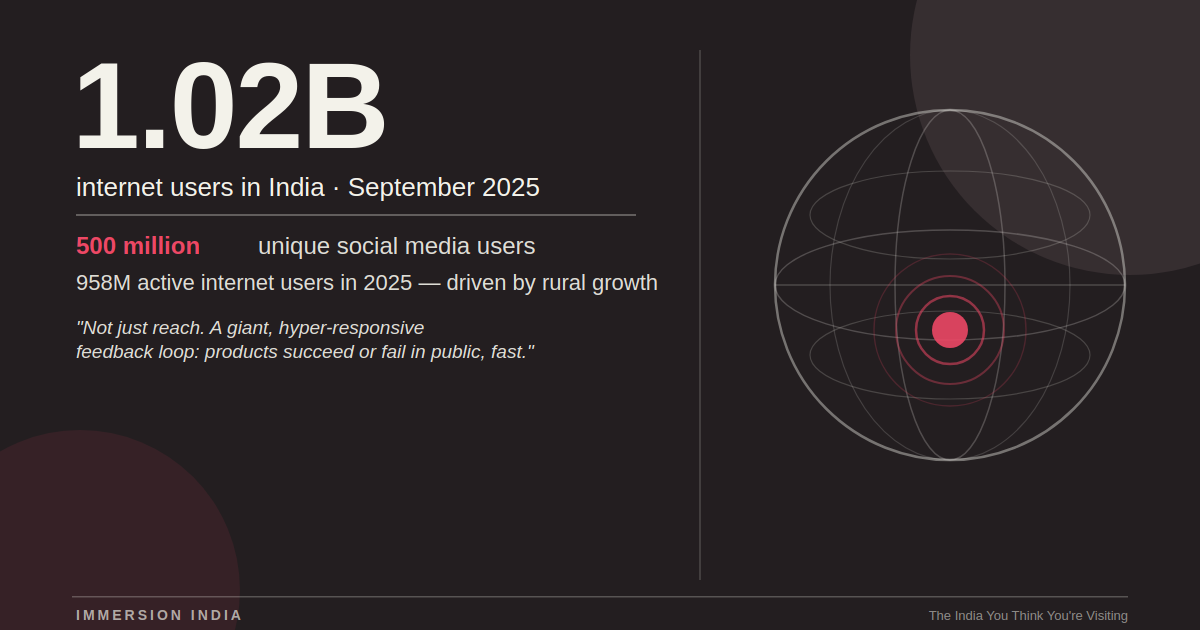

Consider the digital footprint alone. Reuters notes India had nearly 1.02 billion internet users by September 2025, alongside roughly 500 million unique social media users, citing DataReportal.

(Reuters) That isn’t just “reach.” It’s a giant, hyper-responsive feedback loop: products succeed or fail in public, fast.

And digital behaviour is no longer “urban elite.” An IAMAI report summary cited by NDTV put India at 958 million active internet users in 2025, driven significantly by rural growth. (www.ndtv.com)

If anything, “low cost” is increasingly the wrong lens. The better lens is value density: Indian consumers and enterprises expect more outcomes per rupee, more speed per process, more convenience per click. That pushes firms into frugal engineering and ruthless prioritisation—not cheapness for its own sake.

Misconception 3: “India is still catching up digitally.”

Reality: in some rails, India is setting the baseline.

Nothing corrects this misconception like payments.

In January 2026, Indians made 21.7 billion UPI transactions worth ₹28.33 trillion (~$307bn), with average daily transactions around 700 million, reported off NPCI data. (The Economic Times)

UPI’s significance is not “fintech adoption.” It is that transaction friction has collapsed across the economy—street merchants, rent payments, school fees, subscriptions, refunds. When payments are that ubiquitous, firms compete on what happens after the ping: dispute resolution, fraud controls, reliability, and customer support responsiveness.

Then come documents. A Government of India note on DPI reported that as of 5 March 2026, DigiLocker had 67.63 crore users (676 million), and by March 2026 950 crore documents (9.5 billion) had been issued through the platform. (Press Information Bureau) This turns verification into a system property. Many visiting executives realise, uncomfortably, that their own internal processes are slower than the rails available to them.

Misconception 4: “India is startup energy; enterprises are slow.”

Reality: innovation is two-speed, but one ecosystem.

Overseas visitors often separate the India story into two neat buckets: nimble startups versus lumbering incumbents. The field reality is messier and more instructive.

The startup layer is now large enough to shape employment and enterprise behaviour. As of 31 December 2025, India had 207,135 DPIIT-recognised startups, credited with 21.9 lakh (2.19 million) direct jobs. (Press Information Bureau) That scale makes startups not merely disruptors, but specialist suppliers of capability, AI tooling, risk analytics, workflow automation, into large firms.

At the same time, large enterprises are not politely waiting to be disrupted. They are building internal AI factories, partnering aggressively, and institutionalising “release cultures” that look more like product companies than traditional corporates. The most interesting innovation often happens between them: startups providing velocity, enterprises providing governance and scale.

Misconception 5: “If it’s digital, it must be frictionless.”

Reality: India shifts friction; it doesn’t abolish it.

DPI compresses some frictions (onboarding, payments, verification). But the friction reappears elsewhere: logistics, fraud, dispute handling, compliance, language, last-mile service quality, and partner coordination.

Take logistics. India ranks 38th on the World Bank’s Logistics Performance Index (2023), and the government itself has highlighted that ranking and the ambition to improve logistics efficiency. (Press Information Bureau) In the field, cohorts discover that delivery promises and service consistency are operational feats, not marketing lines especially outside top metros.

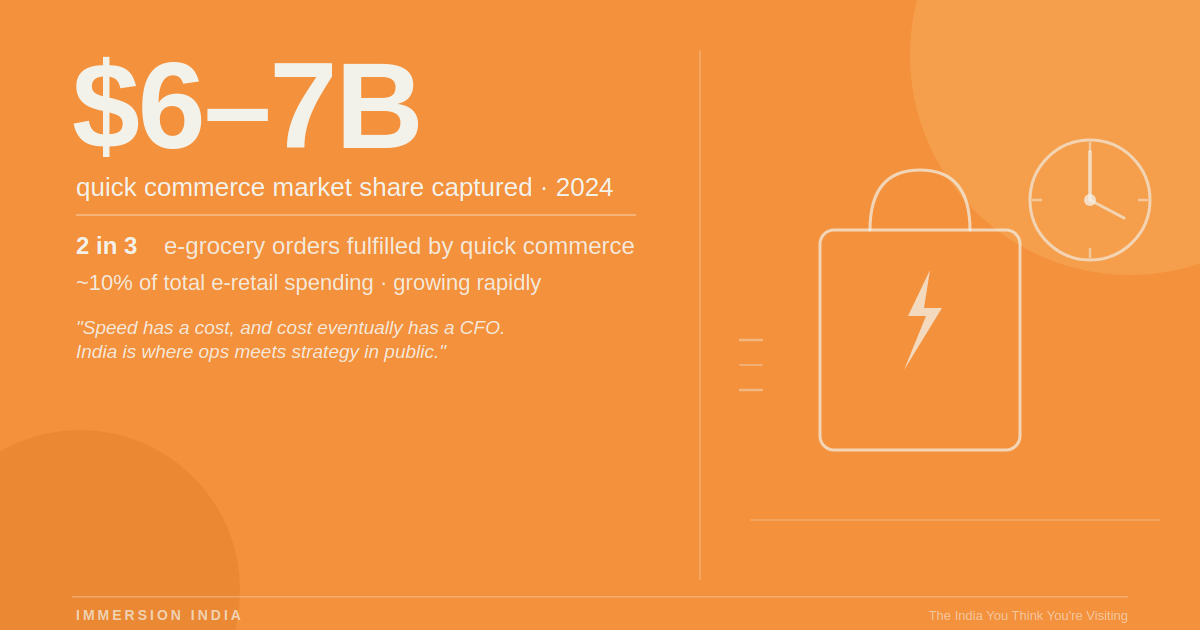

Or take quick commerce. Reuters reported India’s quick commerce captured $6–7bn in market share in 2024, accounting for over two-thirds of e-grocery orders and about 10% of total e-retail spending, growing rapidly but facing profitability questions.

(Reuters) This is innovation at scale and also a reminder that speed has a cost, and cost eventually has a CFO.

The teaching point for executives: India is where ops meets strategy in public. If your operating model is weak, growth does not hide it; it amplifies it.

Misconception 6: “Regulation will either block everything or be ignored.”

Reality: India is experimenting with speed and guardrails, in plain sight.

Visitors often arrive with caricatures: either India is over-regulated and slow, or it is chaotic and permissive. The lived reality is more nuanced: regulation is becoming a design constraint, sometimes enabling, sometimes constraining, always shaping how products scale.

India’s Digital Personal Data Protection (DPDP) Rules, 2025 were notified on 14 November 2025, operationalising the DPDP Act, 2023, per government releases. (Press Information Bureau) This forces organisations to translate privacy into operating practice namely data inventories, consent flows, retention discipline, vendor governance, work that visiting executives recognise from Europe, but at India’s scale and complexity.

Equally instructive is that India is not a one-way street of state power. Reuters reported that a proposal to have smartphone makers preload an Aadhaar app faced pushback from industry groups citing costs and security concerns. (Reuters) The misconception that “the government will simply mandate and it will happen” doesn’t survive contact with the ecosystem.

Misconception 7: “India is mainly a consumer story.”

Reality: it is also a platform, manufacturing, and systems story.

A cohort that only visits consumer brands comes home with a partial picture: aspirational consumption, fast commerce, youthful demographics. Useful, but incomplete.

India’s deeper story is increasingly about systems which are digital rails, supply chains, manufacturing clusters, and enterprise capability. Even logistics and public digital platforms (payments, documents, identity utilities) are reshaping B2B operations and procurement norms. That changes what “competing in India” means: not just selling to consumers, but building with local partners, adapting operating models, and designing for scale under constraints.

What immersion corrects and very quickly

A well-designed field immersion does not “show India.” It tests the cohort’s assumptions against reality:

- Assumptions about uniformity collapse when state-level differences show up in execution.

- Assumptions about cost collapse when customers demand high value and instant resolution.

- Assumptions about digital maturity collapse when UPI and DigiLocker feel like utilities.

- Assumptions about innovation collapse when enterprises and startups ship together.

- Assumptions about regulation collapse when governance becomes part of product design.

India is not an easy place to visit as a manager, because it refuses to fit the tidy mental models executives bring from home.

That is precisely why it is such a useful management laboratory. India does not offer comfort. It offers calibration.

And it starts, often enough, in a traffic jam and quickly followed by a QR code at a tea stall that works flawlessly.